Last week, we discussed how to reconcile your checking account based on your projections. This week, we will begin reconciling the savings account a...

Last week, we learned how to use our spreadsheet to build a savings account or rainy day fund. This week, we will use our spreadsheet to reconcile o...

Now that we have our savings account created and have determined our saving schedule, we can use our spreadsheet to predict how long it will take to b...

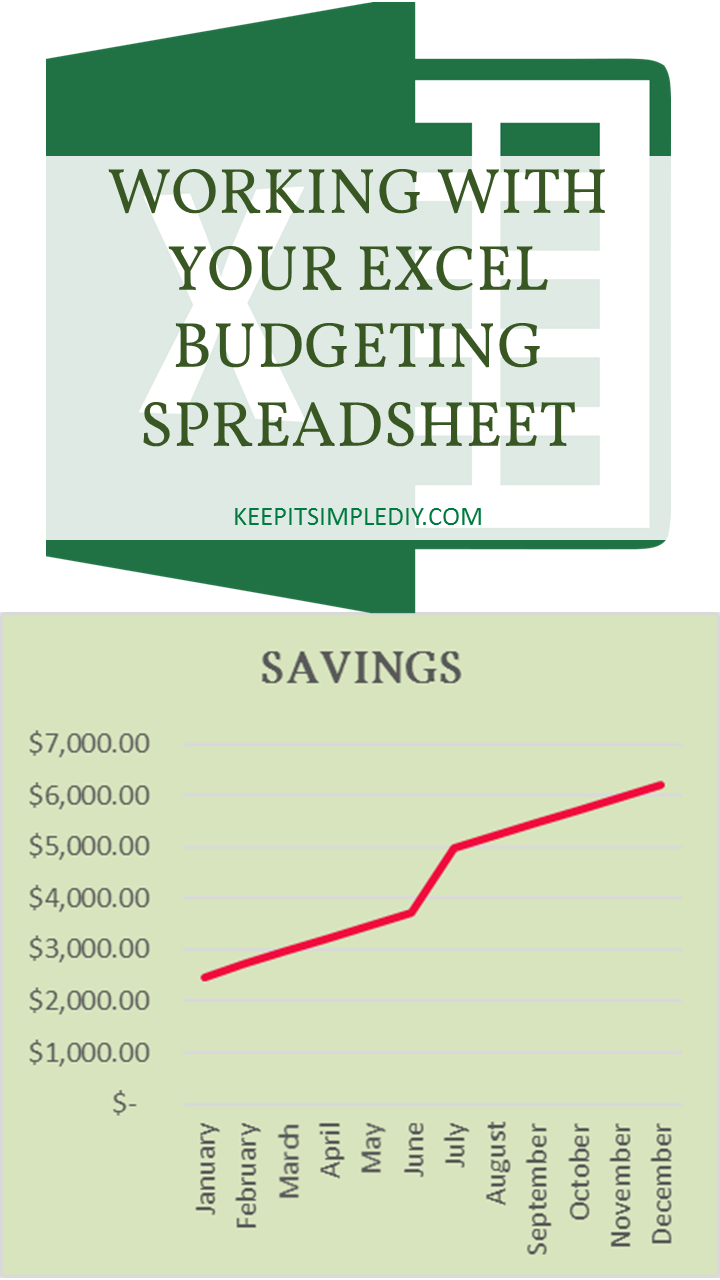

Last week we made our spreadsheet a bit more robust by adding in a Checking account and Savings account rows. If you need to review, you can find th...

I would consider myself to be a modest couponer. I am cautious about the sales and coupons available but do not go overboard stocking my cabinet wit...