This post is part of a series. To start the series from the beginning, click here. To browse through the series, click here.

Let’s recap on reverse budgeting and the cash system.

Reverse Budgeting

Reverse budgeting is a three-step savings process. The first step is to determine how much money you want to set aside each month for savings. If you aren’t ready to start putting money into savings yet, no problem. You can still use the model and implement saving when you are ready.

You will also want to create your spending goals or budget for each category at the beginning of the period. A period can be a pay cycle, a month, or any time period that fits your budgeting needs.

Your budget will need to be reviewed periodically and adjusted as necessary.

Budgeting Tools

Envelopes

The first budgeting tool we will discuss is Envelopes. You can either use digital or physical envelopes for your budgeting system.

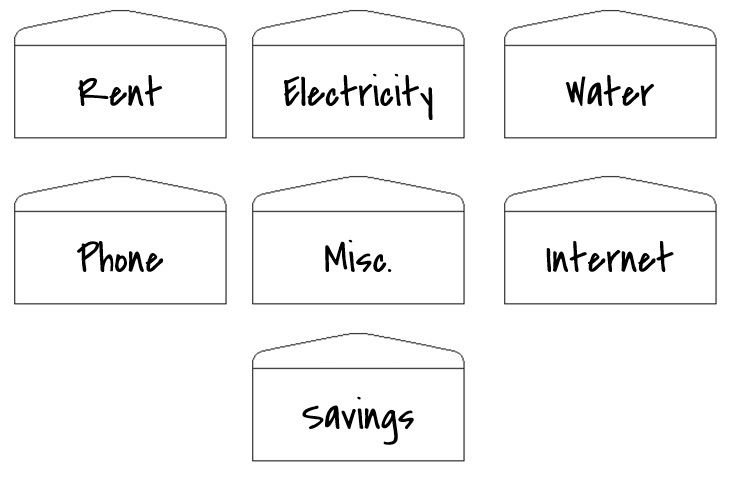

Create an envelope for each of your spending and saving categories.

These are the expenses from the previous example. Note that with the cash system, there is no use of credit cards. Instead, we will change the credit card bill to a miscellaneous envelope.

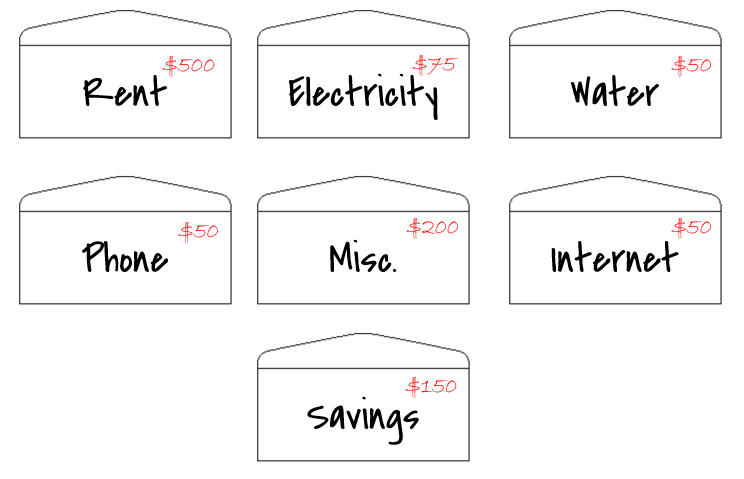

Rent – $500 – 1st of the month

Electricity – $75 – 10st of the month

Water – $50 – 15th of the month

Phone – $50 – 15th of the month

Miscellaneous – $200 – 20th of the month

Internet – $50 – 20th of the month

Total monthly expenses: $925.00

In this example, we will create seven envelopes.

Cash System

The cash budgeting system is cash only. You shouldn’t use credit or debit cards with this system. Of course, you can still use bank accounts to store your savings or have your paychecks deposited if you would like. The main point of the cash based system though is that you cannot over-spend because you physically don’t have the funds to do so.

You can also note the amount due for each envelope. Determine your savings goal based on your income.

The income from the previous example is $562.20 every other week. This means that on a month with two paychecks you make $1124.40. A good savings goal is $150. This gives you a little wiggle room of around $50 but still ensures that you are saving. Note that twice a year you will have three paychecks and will need to adjust accordingly.

Rather than dive right into budgeting in two week periods, let’s start with something more simple. Using a month as a period is the most straight-forward for planning. At the beginning of the month, plan out the budget for each of your envelopes.

Since you have about $50 extra as a buffer, you can choose where you would like to put these funds. You can add them into the savings, add them to another envelope, or just hold them off to the side to use in case you over spend a bit.

Yes, it does sound counter-productive to overspend in a category but habits are hard to break. Just because you have a budget doesn’t mean that you will be 100% faithful to your budget at first. It is good to have a little buffer to help smooth the transition into budgeting. Once you are past the learning curve, you can opt out of having this buffer.

Now that you have your envelopes labeled, fill the envelopes with cash. Throughout the month, use the cash from the corresponding envelopes. At the end of the month, you should be left with the money in the savings envelope. If you are lucky, you will also end up with the buffer money that you can add to your savings envelope. Well done!

A two-week period uses the same technique as the month long period. The only big difference is that you need to plan your budgeting out a bit more in order to have enough money at each billing date based on the date you get paid. Use the money from your paycheck to fill as many envelopes in chronological order as you can. Make sure that the next pay date is before the next envelope without money. This way you will be able to fill that envelope with the next paycheck prior to the expense being due.

You can also have a digital envelope system. You can create envelopes like the ones in my example with a simple graphic. Write your budget on your digital envelopes. This time, instead of filling the envelopes, put your cash in a safe place and only take the amount you need at a time.

Let’s say it’s time to pay the electricity bill. Take $75 out of your money stack and put it towards the bill. Note on the envelope that the money has been spent by using an X over the funds.

This technique is a bit harder to track, especially with the miscellaneous folder. The most important thing is to be pro-active. If you are going grocery shopping, take a small amount of money out of your stack and note the deduction on your envelope. If you don’t spend as much as you planned to, you can add the money back to your stack and add the amount back to your digital envelope.

Paper/Check Register – Printable

There are many ways to create a register. You can use a register booklet typically found in the top of a checkbook. You could also make your own tracking sheet by using a way to track your finances that makes the most sense to you.

There are many sites online that explain how to balance your register booklet so I will not be going into the details.

Instead, I will focus on some customizable options for tracking your spending.

The best place to find budgeting printables is Google Images. There are many in a variety of different colors and formats.

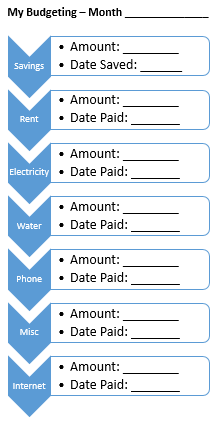

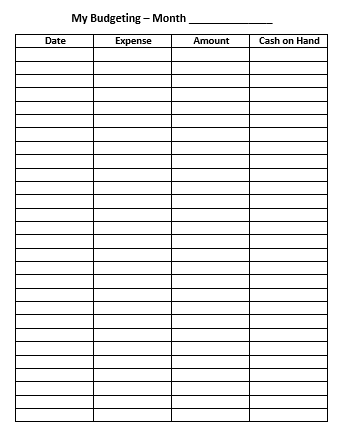

Here are two very different styles. The first tracking device is more of a checklist. To use this, you would plan your budgeting at the beginning of the period and update the amount of each expense. Once you make the payment, add the date to the date paid section.

This form tracks a bit more information. Start by creating a line for the starting date for your savings amount. Put that amount aside the total how much cash you have on hand. Remember, this is the most important part of Reverse Budgeting, saving first.

Every time to take money out of the stack, write down what the money was for and how much. Then, subtract the amount from the previous cash on hand balance. This helps you know exactly how much cash you have left at all times.

Computer Spreadsheet

We just created a tangible tracking sheet for your spending. If you prefer, you could create the exact same tracking sheet in a spreadsheet such as Microsoft Excel or Google Docs. This would allow you to check your budget from the computer or even on your phone if you have cloud based documents.

Apps/Programs

It is definitely possible to use apps and programs with a cash system. However, for many, the apps may be too complicated or have too many options. For this reason, I am going to leave forgo the topic of apps and programs for the cash system. Not to worry though, I will be discussing apps and programs in the digital section.

These are great tips for not living paycheck to paycheck as we do. I’ll be taking note of this in the New Year.

Great tips for budgeting, will have to share this one with my daughter and see if it helps any. she has such a hard time saving.

I’ll adopt this envelope system. I need a push to be more disciolined in savings.

It’s hard to save when you get behind especially. That’s where we’ve been at for months.. just can’t seem to get ahead. Will be looking at this hard for the new year. Thanks for step by step for the cash method!

Those are great tips.There are various ways to make our income work for us. I heard of the envelope idea before. I’m not quite sure which method would work best for me, but I have some time to think it over lol. Thanks for sharing!

What a great post. So much info so i can budget and plan for 2017. Thanks!

Useful ideas. If you keep a record of your money, you can tell it where to go!

Reverse budgeting and the cash system sounds very interested. I used to be such a good saver before my kids turned into teenagers. Now they are in need of so many things because they are involved in sports and activities. Also, saving is a little hard when I have 3 kids to put through college. Hopefully someday I will be able to put more money aside in the future.

I love being financially responsible and the tips you shared are something that I can attest to. I’m sure it will help many. Happy 2017!

I love the cash method. It’s so easy and really starts to show you how much you overspend.

This is a great idea I’m going to show this to my girlfriend.

http://sheismelrose.net/

These are great tips – I’ve used the envelope system successfully before and I loved how efficient it was.

Shared this with the hubby and bookmarked. Wow! Thanks for sharing!

I think this a great blog! Perfect for people trying to save money like me!

Great ideas, thanks for sharing

Thanks for these tips. They’re bound to help.

Very informative blog post. I know my husband and I will be working to get out of debt starting March. Since we will be down one car note and almost 200 a month on car insurance yay.

some great tips and tools here – thanks so much!

Great system you have going. We’ve never had to live pay check to pay check. We have always been very good with budgeting.